Failure of Old Economic Solutions

Update Jan 28, 2025. I am not optimistic that tariffs and austerity will not induce a significant economic slowdown within the next 2-3 years.

President Trump is threatening allies, non-aligned countries, and BRICS nations with tariffs almost every day. Meanwhile, with the Department of Government Efficiency (DOGE) and the executive order to freeze all government loans and grants, we are facing governmental austerity.

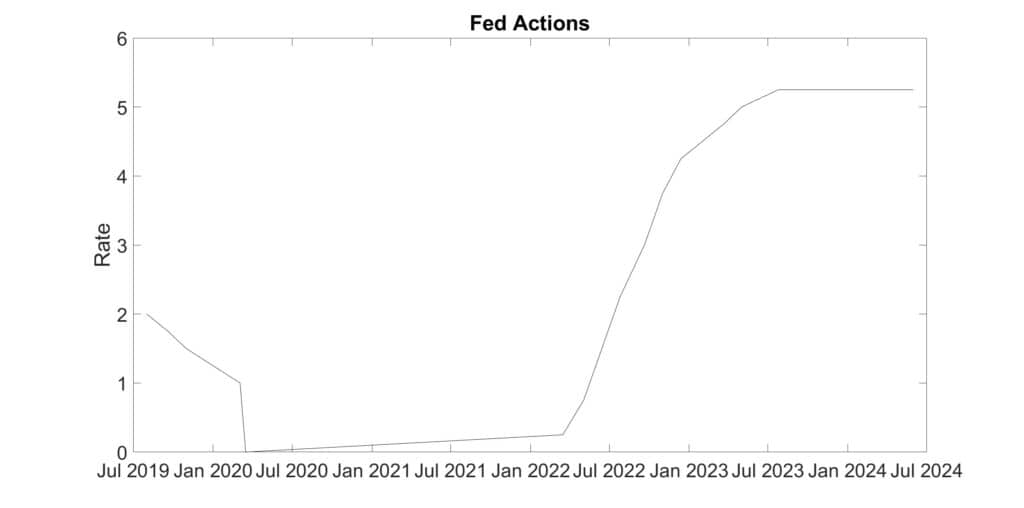

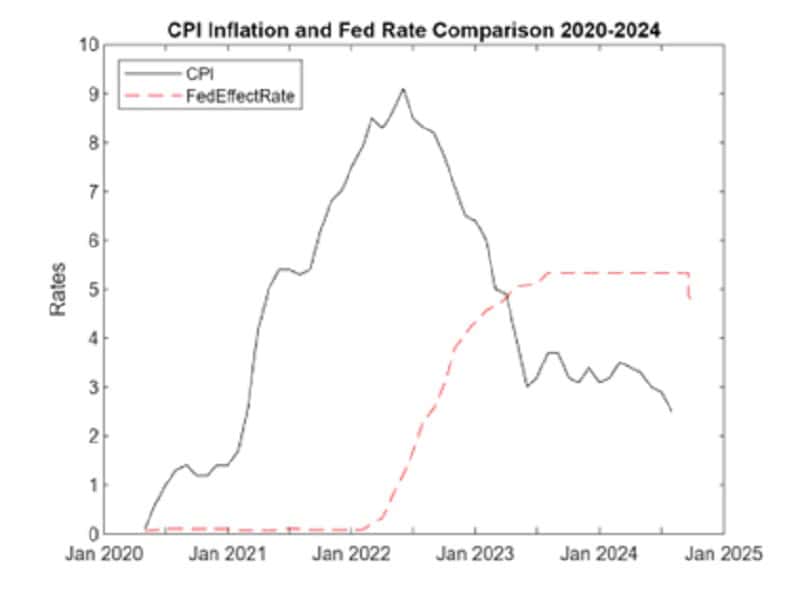

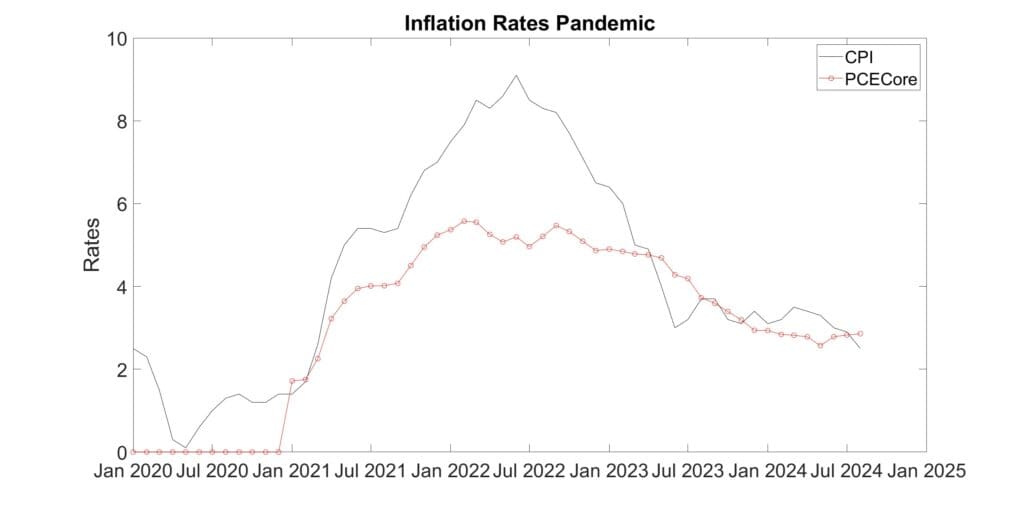

The economy is strong now, despite the worrisome Federal debt. Tariffs are being used as a bully stick against countries that don’t act as Trump wants them to. He ignores economic consequences that are contrary to his favored worldview, believing the United States has done all the work of peace and security without getting sufficient return from allies and other countries.

The United States has seen this combination of tariffs and austerity before. During the Great Depression, it had a terrible impact. Fortunately, during the 2007-2008 housing debacle, that approach was not taken.

I am pessimistic. Tariffs and austerity are likely to cause a painful economic recession within the next year or two.

In this Great Recession, the economy is rotten and no one knows what to do. They are trying, but failing.

In the 1930s when it was like this before, it didn’t end until bigger worries overshadowed the economic problems of low demand and declining prosperity. The policies of increasing of tariffs and austerity programs made the Great Depression worse.

Currently, we have two main problems—loss in confidence in government and financial institution to solve the bursting of a housing bubble that has sapped discretionary consumption and increasing globalization which puts downward pressure on our living standard that was built upon isolated markets.

For the first problem, the US should allow everyone who is current on their mortgage to refinance, even if their mortgage is underwater (to the new, lower valuation).

For example, a $350,000 mortgage on a house currently assessed at $250,000 would get broken into 2 mortgages. The $250,000 mortgage will be at a new lower rate. The $100,000 would continue at the older, higher rate. The home owners are already paying on their mortgage. The risk to the loan maker is not increasing. It is decreasing. It helps the home owner and the economy by freeing cash for non-mortgage consumption.

Although it’s not pleasant, the second problem of globalization eroding United States workers standard of living is being accommodated by inflation in food, education, and healthcare. That is painful, but it also helps. Money from those expenditures stay in the US, raising the living standards for agricultural workers, college staff, and medical personnel.

Image by Dominic Alves from Brighton, England – Northern Rock Queue, CC BY 2.0, https://commons.wikimedia.org/w/index.php?curid=2759713