Inflation During Tariff Semi-Pause

Update 2025.04.13 Trump exempted Apple’s iPhones and other tech from the 145% China import tariff. Those imports will still be subject to the prior 20% tariff, unless Trump decides they are not. This action does not substantially change the inflation estimate in this post; however, it’s a clear example of the government’s willingness and ability to favor particular companies.

Despite a pause in “reciprocal” tariffs under Trump, significant tariffs remain in place. These include a blanket 10% on all imports, 145% on imports from China, and 15% on auto, steel, and aluminum imports.

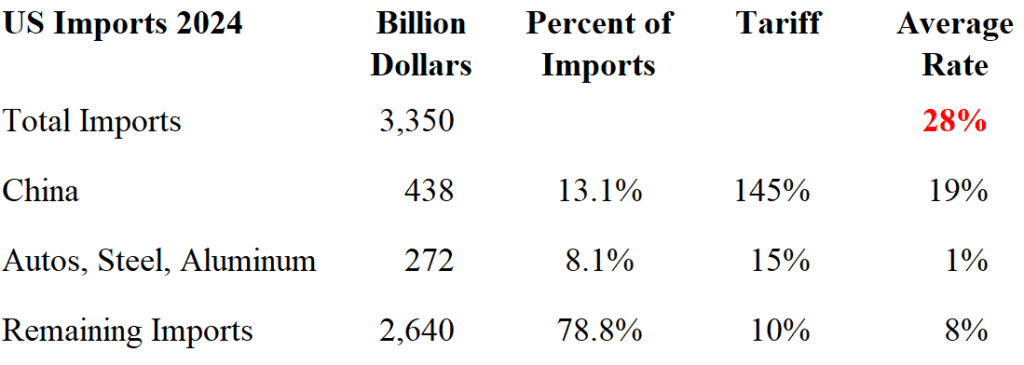

Sticking to the current situation, let’s calculate the average tariff rate to estimate its impact on U.S. inflation. The figure below, a snapshot of an Excel spreadsheet, demonstrates the relative amounts of imports at different tariff rates, leading to an average tariff rate of 28%.

Immediate Impact on China-to-U.S. Imports

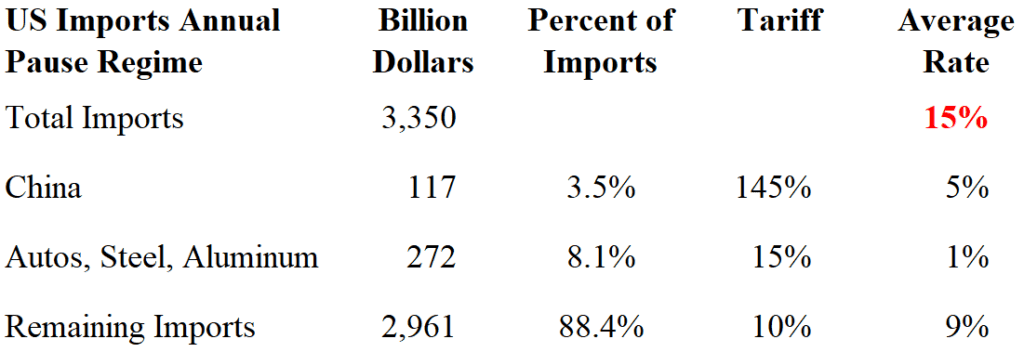

Since the 145% tariff on imports from China more than doubles the price of Chinese goods, we can expect imports from China to drop significantly, perhaps by 75%. While some items, such as high-demand products like iPhones, may still need to be imported because of their unique production requirements, most goods previously sourced from China are likely to switch to other countries with the 10% tariff. Over time, it is possible that some goods may even be sourced domestically.

Using the 75% estimate for the decline in China-to-U.S. imports, the figure below illustrates how the experienced tariff rate falls to 15%, as imports shift to countries with lower tariffs.

Inflation During Tariff Semi-Pause

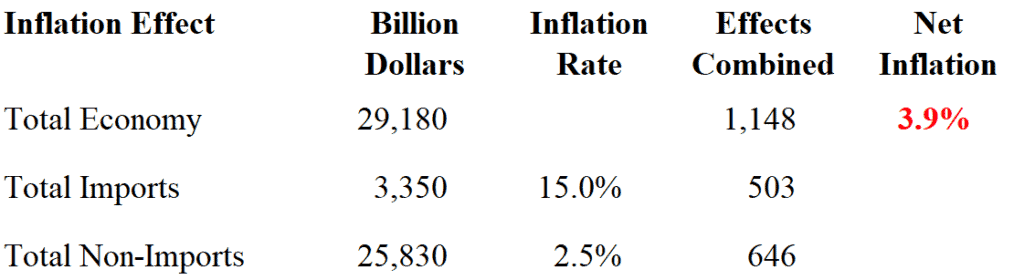

The 15% price increase on imports will predominantly be passed on to consumers. Because of stockpiling and warehousing, the inflationary impact is likely to stretch over several months, gradually diminishing as businesses and consumers adjust to price increases. This analysis assumes the current tariff situation remains unchanged. The figure below shows the contribution of tariff inflation augmenting existing inflation.

With the Federal Reserve’s target of 2% inflation, nearly doubling the experienced rate to 3.9% presents a significant challenge. Raising the benchmark rate is the Fed’s primary tool for combating inflation, but this approach risks further slowing an already weakened economy.

Of course, the Fed’s dilemma pales in comparison to the strain felt by American households, as families are forced to stretch their budgets to afford everyday necessities amid rising prices.

Additional Information

Tariffs and Stagflation