The Fed, Inflation, and Unemployment

How did the Federal Reserve Board perform on its dual mandate of low inflation with full employment since the COVID-19 pandemic?

Why even consider the pandemic in an economic discussion?

The COVID-19 pandemic significantly disrupted economic activity in early 2020, causing unemployment rates to spike. In response, the Federal Reserve swiftly lowered its Funds rate to counteract the economic slowdown2. However, by late 2021, inflation began to rise, prompting the Fed to increase the rate in March 2022 to curb price increases.

Pandemic and Aftermath

Fed Fund Rates

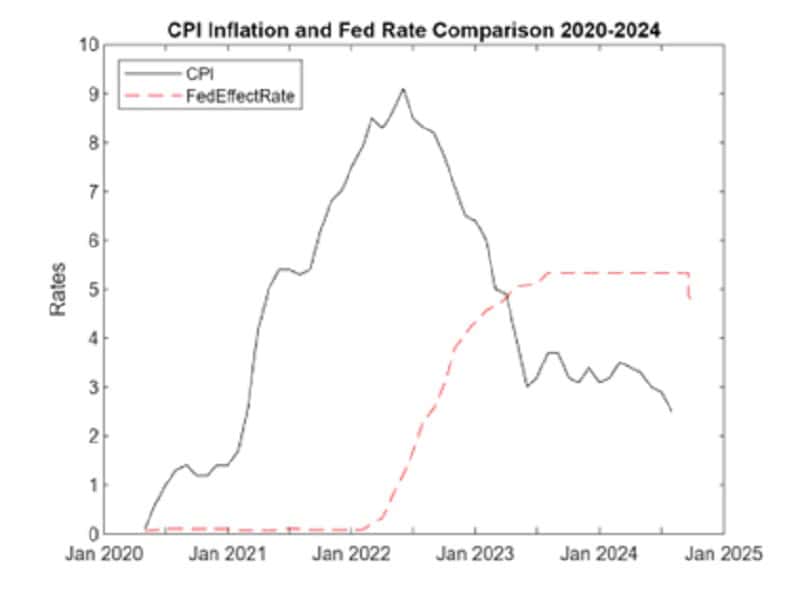

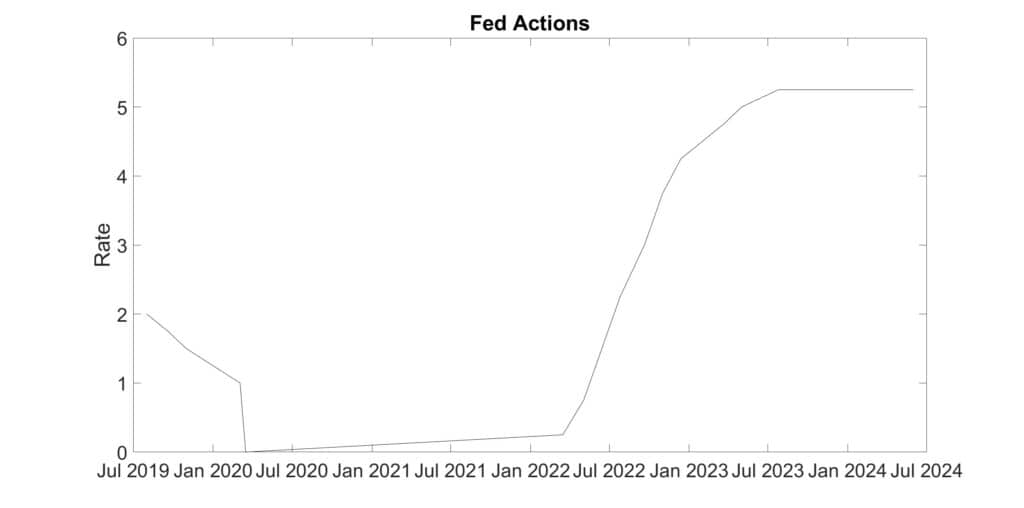

The Fed Rate plot (above), spanning from September 2019 to September 2024, highlights the dual conditions the Federal Reserve is tasked with addressing. At the beginning of this period, the Fed dropped the Funds rate to nearly 0% to mitigate the unemployment spike caused by the initial shock of the pandemic, making money easier to access. Then, in March 2022, the Fed initiated a series of Funds rate increases in response to rising inflation.

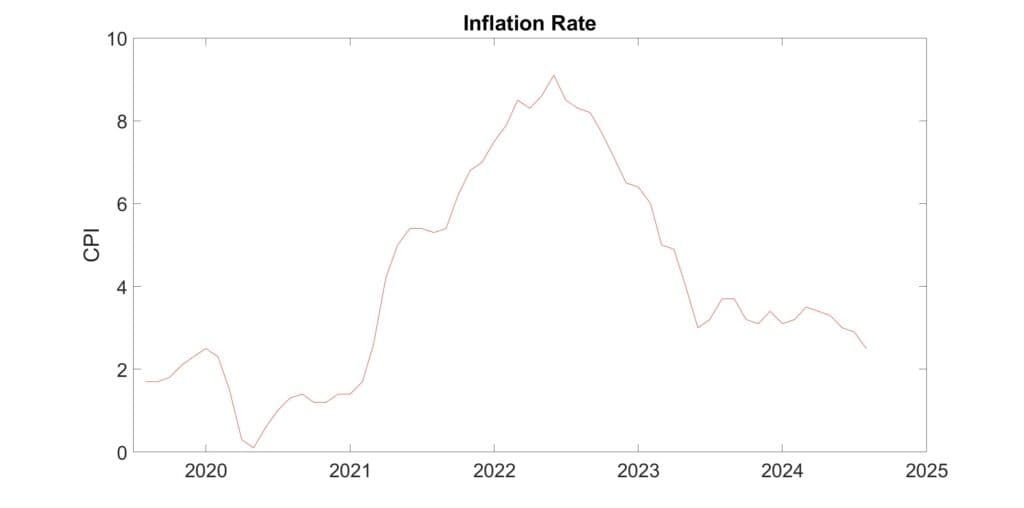

Inflation

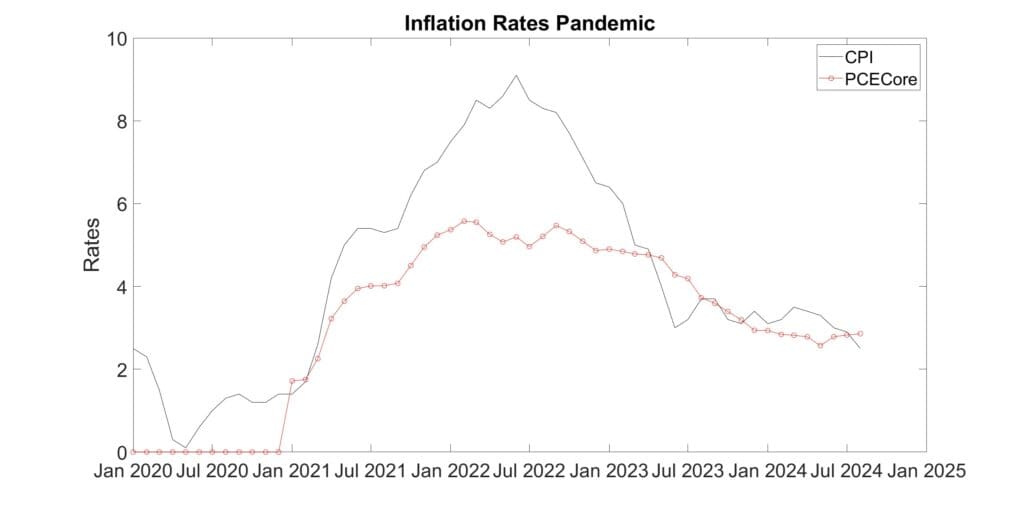

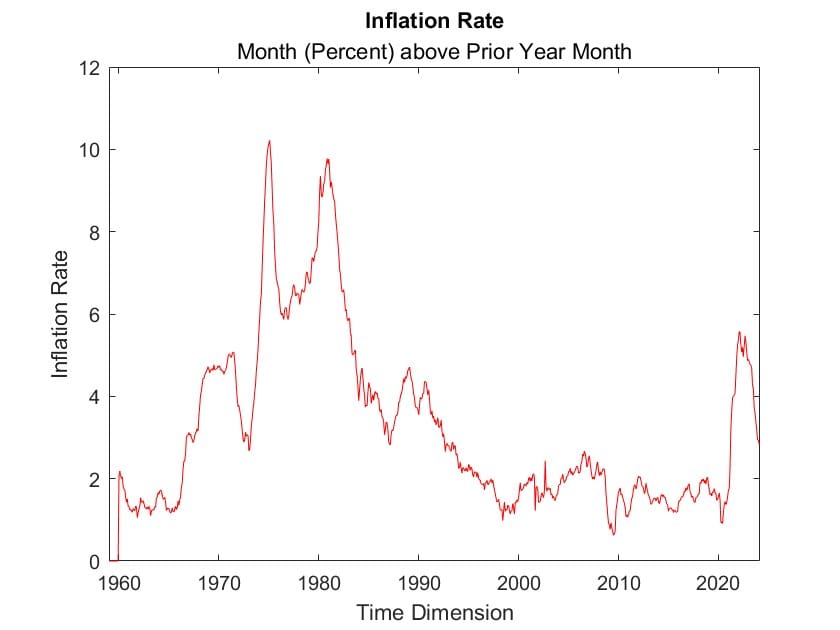

Over the period of the Fed’s actions, inflation (plot below) behaved as follows: The annual inflation rate remained below 2% until early 2021, which was beneficial as easy money policies addressed unemployment concerns. However, by early 2022, inflation had rapidly risen to 7%. The Fed did not respond to this concern until March 2022, when it began raising the Funds rate. Over the following two years, inflation declined to under 3%. Some might argue that the Fed’s response was delayed. Now, let’s consider the changes in the unemployment rate.

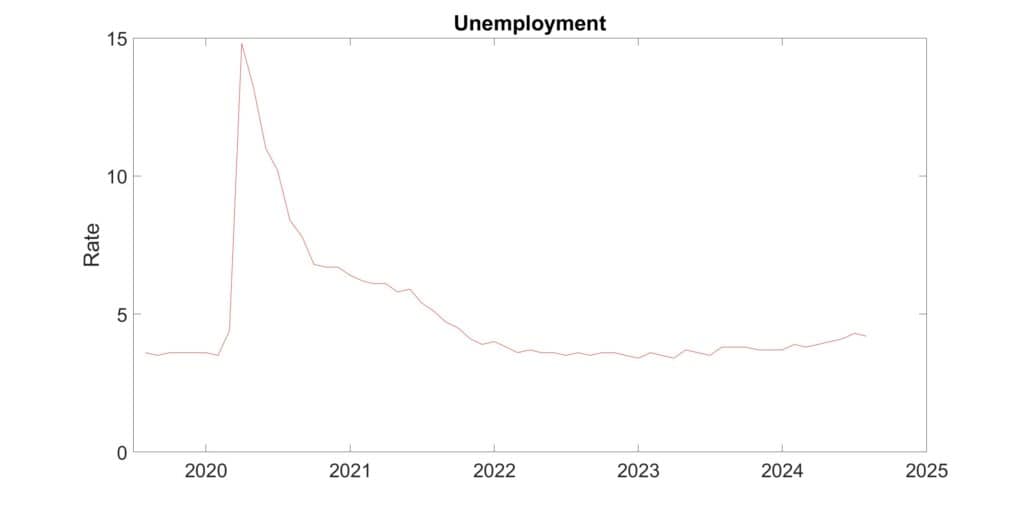

Unemployment

Unemployment (plot below) spiked to nearly 15% in early 2020. In response, the Fed lowered its interest rate to ease borrowing and stimulate business activity (a monetary response). Additionally, Congress and the President enacted legislation to provide relief to individuals and small businesses, helping them stay afloat (a fiscal response).

By early 2021, the unemployment rate had halved, and by the start of 2022, it was down to 5%. Some argued that with unemployment at this level, addressing inflation was feasible.

Fed Performance since 2020

The Fed had two rate cycles during this period. The first was to lower rates and ease business conditions during the economic shock, and the second was to hike rates and reduce inflationary pressures. Combined with the fiscal measures mentioned earlier, the economic shock was difficult to endure but short-lived. Although the Fed’s response to inflationary pressures was somewhat delayed, the continuation of fiscal policies contributed to more money chasing a fixed economic output, making inflation more persistent.

As a result, the Fed’s performance is somewhat muddied by legislative actions that prolonged inflationary pressures. On the whole, however, the Fed’s performance was commendable—mitigating the pandemic downturn and reducing inflation, although it cannot undo the increased costs that the early inflation spike imposed on consumers.

Deciphering the Rate Changes by Fed Policy Cycle

In each of these cycles, the Fed adjusted rates in response to prevailing economic conditions, aiming to manage inflation and unemployment. The “Date Start” marks the first rate change in the cycle, while the “Date End” indicates the final rate change. The “Date Turn” is the day before the Fed reverses its direction of rate changes, allowing the prevailing rate to impact the economy until then.

| Regime | Purpose | Type | DateStart | DateEnd | DateFedTurn |

|---|---|---|---|---|---|

| Dot Com into Post 9/11 | to help econ | falling | 2001-01-03 | 2003-06-25 | 2004-06-29 |

| Housing Boom | to stop inflation | rising | 2004-06-30 | 2006-06-29 | 2007-09-17 |

| Great Recession | to help econ | falling | 2007-09-18 | 2008-12-16 | 2015-12-16 |

| Return to Normalacy | to stop inflation | rising | 2015-12-17 | 2018-12-20 | 2019-07-31 |

| Stimulus then Pandemic | to help econ | falling | 2019-08-01 | 2020-03-16 | 2022-03-15 |

| Taming Inflation | to stop inflation | rising | 2022-03-16 | 2023-07-25 | 2024-09-19 |

By analyzing these rates, we can gain insights into how the Fed’s policy actions influenced inflation and unemployment over time.

Let’s delve into how the Fed’s rate changes influenced unemployment and inflation over different policy regimes.

| Regime | Purpose | Fed Start | Fed Stop | Unemp Start | Unemp Stop | Unemp End | Inflat Start | Inflat Stop | Inflat End |

|---|---|---|---|---|---|---|---|---|---|

| Dot Com into Post 9/11 | to help econ | 6.50 | 1.00 | 4.2 | 6.3 | 5.6 | 3.5 | 2.1 | 3.3 |

| Housing Boom | to stop inflation | 1.00 | 5.25 | 5.5 | 4.6 | 3.7 | 3.0 | 4.3 | -1.3 |

| Great Recession | to help econ | 5.25 | 0.00 | 4.7 | 7.3 | 5.0 | 3.5 | 0.1 | 0.7 |

| Return to Normalacy | to stop inflation | 0.00 | 2.25 | 4.8 | 3.9 | 3.7 | 1.4 | 1.9 | 1.7 |

| Stimulus Then Pandemic | to help econ | 2.25 | 0.00 | 3.6 | 4.4 | 3.6 | 1.7 | 1.5 | 8.5 |

| Taming Inflation | to stop inflation | 0.00 | 5.25 | 3.7 | 3.5 | 4.1 | 8.3 | 3.2 | 2.4 |

Dot.Com Crash and 9/11 Aftermath

In the Fed’s first policy regime of the Dot-Com crash and 9/11 aftermath, the Fed dropped its rates from 6.5% to 1.0%. During this period, the unemployment rate rose from 4.2% to 6.3%, before dipping to 5.6% as rates were raised for the Housing Boom. Unemployment initially jumped by 50% of its starting level when the Fed stopped raising rates, eventually drifting down to a net increase of 33%.

Although this result may not appear positive, it is important to consider that unemployment might have been even higher without the Fed’s easing of its Funds rate. Meanwhile, inflation decreased as Fed rates were rising and eventually returned to nearly the same rate experienced at the start of the cycle.

Housing Boom

The second policy regime emerged when excess, easy money was lent to improperly vetted new home buyers. This influx of money into the general economy led to inflation. To counteract this, the Fed increased its rates from 1% to 5.25% over two years, from 2004 to 2006, and maintained a high level through most of the third quarter of 2007. During this period, inflation rose from 3% to 4.3%, but it fell to -1.3% when the Great Recession hit, demonstrating the severity of the economic downturn.

The Fed’s strategy to combat inflation was effective; moreover, the unemployment rate actually decreased during this period. This regime underscores the Fed’s ability to manage inflation even as it faced significant challenges within the housing market and broader economy.

Great Recession

During the Great Recession, the Fed acted decisively to boost the economy as the cascading failure of companies threatened not just the U.S. but many other economies worldwide. The unemployment rate surged from 4.7% to 7.3% over a year and three months, during which the Fed reduced rates from 5.25% to 0%. However, it wasn’t until 2015 that the unemployment rate fell back to 5%, just slightly above the level at the start of the Great Recession in 2008.

It’s important to note that the Fed and its monetary policy are not the sole influencers of economic activity. Congress and the President also played crucial roles through legislation that provided grants and bailouts for banks, financial lenders, and even automobile manufacturers. Additionally, tax laws were adjusted to stimulate demand and boost the economy, representing fiscal policies distinct from the Fed’s monetary policies.

Return to Normalacy

This Fed regime was not specifically aimed at fighting inflation or promoting economic growth. Instead, the goal was to tighten the money supply without increasing unemployment, thereby giving the Fed room to cut rates if the economy slowed again. Over three years, the Fed gradually inched rates up. As the table shows, the unemployment rate did not rise; in fact, it fell from 4.8% to 3.5%.

This was a notable achievement, complemented by the inflation rate remaining below 2%.

Fed Performance this Century

The Federal Reserve has done a commendable job managing monetary policy over the past quarter-century, navigating numerous external shocks that have impacted the economy. From the Dot-Com boom and 9/11, through the recklessness of the housing boom, to the long slog through the Great Recession, followed by a global pandemic that unleashed a torrent of money for limited production, igniting inflation—the Fed has faced them all.

While no one could manage a perfect record under such conditions, given the uncertainty and limited tools at its disposal, the Fed’s performance deserves a solid B+. This is a remarkable achievement considering the complex and unprecedented challenges it has had to tackle.

f Trump brings the Federal Reserve under direct political influence, it risks becoming like our fiscal policies—focused on immediate reelection concerns rather than long-term economic stability. This shift could lead to monetary decisions that prioritize short-term gains at the expense of future consequences, undermining the Fed’s ability to manage inflation and unemployment effectively. The independence of the Fed is crucial for making unbiased, data-driven decisions that benefit the economy in the long run, rather than being swayed by the political climate of the moment.