The Lane Between Wall Street and Main Street

Update Apr. 2, 2025. Tariffs and the 2017 Tax Extension compel a relook at the results of the 2017 Tax Cut and Job Act.

Update Aug. 25, 2022. The Tuition Loan Forgiveness is an example of a Bottom-Up policy mentioned in the post. The entire economy will benefit.

The terms “Wall Street” and “Main Street” are staples of political and economic discussions, yet their differences often remain unclear. How do they diverge, and how do governmental policies impact them uniquely?

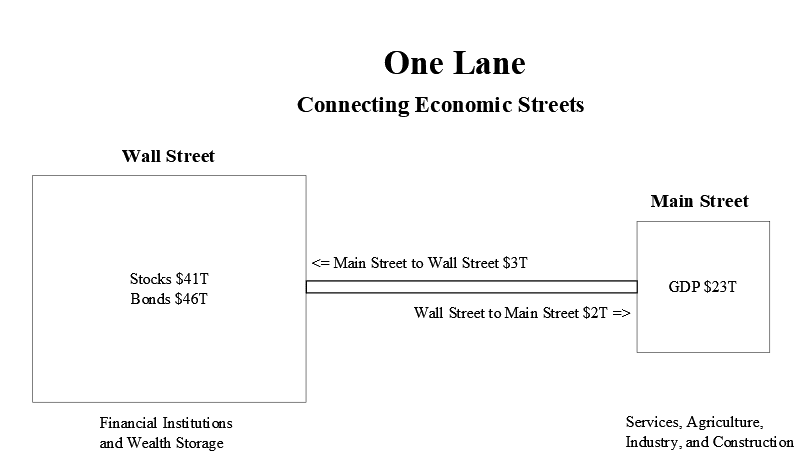

Main Street represents the heartbeat of everyday economic activity, captured by GDP. It encompasses workers, factories, retail outlets, services, and consumers. In 2021, the scale of Main Street was immense, with GDP reaching $23 trillion.

Wall Street, on the other hand, is the engine of ownership and financing for economic activity. It mirrors past achievements and anticipates future opportunities. Wall Street includes the NYSE, Nasdaq, commodity markets, banking, and insurance systems. In 2021, the combined capitalization of the US stock market ($41 trillion) and bond market ($46 trillion) amounted to a staggering $87 trillion. For Americans, Wall Street serves as a repository of wealth through stocks and bonds.

The connection between these two streets is a dynamic flow of money. Net profits from GDP, totaling $3 trillion in 2021, move from Main Street to Wall Street. Meanwhile, Wall Street channels investments—$2 trillion in 2019—back into Main Street, fueling growth through past profits and loans. Curiously, the smaller Main Street generates the funds that sustain the larger Wall Street.

With this foundation in place, let’s explore how two recent policy changes have shaped the relationship between these two economic powerhouses.

Tax Reduction Impact

The 2017 Tax Cut and Jobs Act (TCJA) reduced corporate tax rates, with promises of making American businesses more competitive globally and boosting economic activity. Forbes, on November 17, 2017, supported this argument, stating:

> “The argument for cutting corporate tax rates is that it will stimulate business capital spending. Greater capital spending increases the economy’s total productive capacity, and it boosts the value of each additional worker. Thus, capital expenditures grow the economy and wages both.”

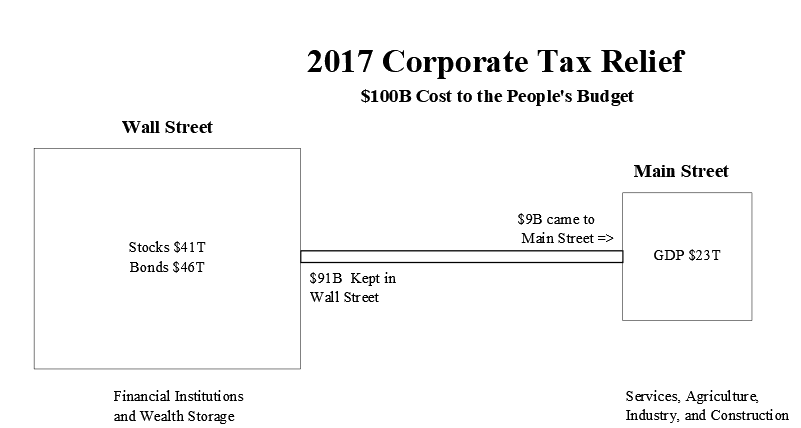

But what actually happened? The corporate tax cut led to a $100 billion increase in corporate profits in its first year. However, the distribution of these gains was strikingly uneven: 91% went to Wall Street in the form of stock buybacks and dividends, while only 9% was allocated to R&D and capital investments that could benefit Main Street.

Forbes revisited this issue on February 21, 2019, highlighting the lack of capital investment:

> “[I]t’s helpful to focus on R&D, because R&D is a leading investment—it creates opportunities. Capital investment then follows to exploit those opportunities. In short, the reason the TCJA didn’t increase R&D investment is that most companies were already over-investing in R&D.”

Instead of driving economic growth, corporations prioritized stock buybacks, triggering executive bonuses. This outcome contradicted the very rationale Forbes had initially used to support the TCJA.

In essence, the “trickle-down” effect gave Wall Street a $100 billion tax break in its first year, of which $91 billion stayed within Wall Street, while only $9 billion trickled down to Main Street. Lower corporate taxes enriched CEOs and benefited the wealthy stockholders, but they failed to significantly boost Main Street—the true pulse of the economy—through job creation, wage growth, or reduced inflation.

Federal Pandemic Rebates

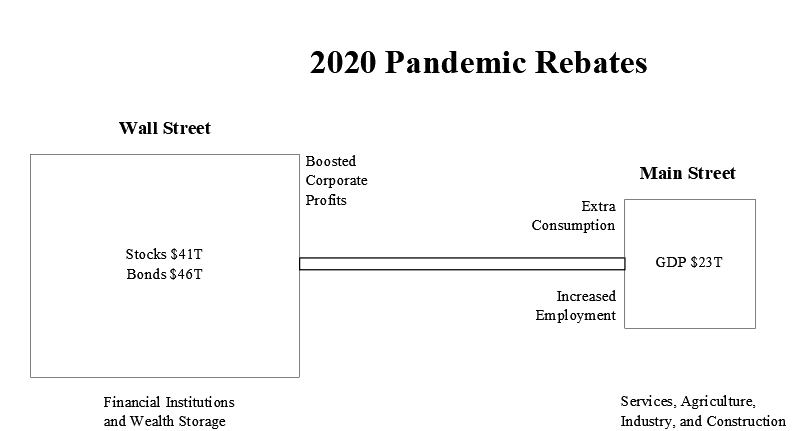

The COVID-19 pandemic brought unprecedented economic challenges, prompting the Federal Reserve to adopt a multi-pronged strategy to mitigate the fallout. One key measure was the issuance of cash rebates to every American. These rebates had a profound impact on Main Street, as the majority of recipients spent the funds on essentials like groceries, personal shopping, and delivery services. This spending rippled through the economy, benefiting wholesalers, manufacturers, and ultimately corporate coffers and Wall Street.

The immediate effect of these rebates was a surge in GDP, as consumer spending fueled job creation and business activity. By 2022, the economy saw historically low unemployment rates and rising salaries—a testament to the effectiveness of this broad-based monetary intervention. The rebates exemplified a “Bubble Up” policy, where Main Street was directly empowered with spending capacity. This spending not only revitalized local economies but also delivered profits to Wall Street, with 13% of the net gains flowing upward.

Future Economic Actions

Bubble Up policies are demonstrably more effective than Trickle Down approaches in addressing challenges across the broader economy.

An equal reduction of the individual tax burden offers a tangible way to stimulate economic growth. Instead of adjusting tax rates across all brackets, providing every taxpayer with a $1,000 tax cut has a direct and widespread impact. The overwhelming majority of recipients spend this extra cash, triggering a ripple effect that boosts economic activity beyond the initial amount. This multiplier effect showcases how money circulates in the economy: the busboy’s increased earnings are spent at local shops, whose proprietors, in turn, invest in goods and services. Each cycle further amplifies incomes and spending, creating a cascading chain of economic benefits.

Ultimately, corporate profits rise, flowing upward to Wall Street—but only after passing through the hands of many along Main Street. By empowering consumers and workers first, Bubble Up policies activate the real engine of the economy, fostering both growth and inclusivity.

The impact of new debt incurred by the legislation is ignored here. Not because it is unimportant to consider, but because it distracts from the different manner by which Wall Street and Main Street react to government policies.

1 thought on “The Lane Between Wall Street and Main Street”